Report a Maintenance Issue

Report a Maintenance Issue

This is the question many people are asking right now, and the answer depends on your circumstances.

I pride myself on my ability to provide objective, fact-based information on the Whickham property market so potential Whickham house sellers, landlords and buyers can make the best decision for themselves.

My role is to educate the potential Whickham house sellers, landlords and buyers and to provide them with the best possible information available, not to convince them to do something they don’t want to do.

To answer that big question in the title of the article (is now a good time to buy a Whickham home?), it comes down to three things.

1. How much will you get for your Whickham home when you sell it?

2. How much will you have to pay for your new home?

3. How much will that move cost you in ongoing monthly mortgage payments?

To answer points 1 and 2 correctly, I need to address point 3, which relates to interest rates.

The click-bait newspapers and websites are pushing messages to potential sellers and buyers towards the top end of the sensationalised scale. I prefer to define what is happening, i.e. the reality.

On the face of it, it doesn't look good.

The average 5-year fixed rate mortgage has risen from 2.11% at the beginning of January this year to 6.21% in early November.

Yet even though the Bank of England increased the base rate by 0.75% on the 3rd of November, the average 5-year fixed rate mortgage dropped by 0.22% between the 3rd week in October and bonfire night. As interest rates go up, mortgage rates are coming down even though interest rates are projected to increase to 4.5% by the autumn of 2023.

So, why did the Bank of England mention in the first week of November that the UK is facing a two-year recession? Some might think this controversial, yet the Bank of England wants a recession as it will aid in reducing inflation. It’s as plain and simple as that!

Instead of relying purely on interest rates to reduce inflation, the Bank of England is hoping if we go into some form of shallow recession, it will not need to increase interest rates much above the anticipated 4.5%.

However, whether it's interest rates or a recession, both will slow the number of home sales in Whickham and will indirectly affect Whickham house prices.

So will Whickham house prices drop? By how much and what money will it save you if you wait?

I have spoken recently in my property blogs about the Whickham property market, and the prices that will be achieved for homes in late 2023/early 2024 will be between 5% to 10% lower than what is being achieved today. There is no point in repeating why (message me if you want those articles), but in essence, increasing mortgage rates, inflation and affordability will mean the price people can pay for a Whickham home will be curtailed because of those factors. Let's assume a reduction of 10% in Whickham house prices.

Around 81 in 100 existing homeowners are buyers. When they sell their home, they almost always move upmarket regarding accommodation and location. Hence, they will pay more for the home they buy than the property they sell.

So, if you are in Whickham and live in a 2-bed house (average value £130,100) and want to buy a 3-bed house (average value £210,300), the difference between both would be £80,200.

If Whickham house prices dropped by 10% in a couple of years, that £130,100 2-bed house would drop to £117,090, and that £210,300 3-bed house would drop to £189,270, meaning the gap would drop to £72,180. Thus, saving the home buyer £8,020.

So, should they wait?

Yes, until you look at the monthly ongoing mortgage payments.

Assuming our Whickham homeowner has an existing mortgage of £100,000 and added the difference of moving up the property ladder to the mortgage. If our Whickham home mover moved now, their mortgage payments would be £948.89 per month (assuming a 35-year mortgage on a 5-year fixed rate at 5.34% with First Direct).

The other scenario would be if our Whickham buyer waited a couple of years for Whickham house prices to drop 10% (to save £8,020 as mentioned above) to make a move.

Everyone acknowledges interest rates will rise in the next two years, so the monthly mortgage payments when they move (even though they are borrowing less) would be £1,123.00 per month (based on a 5-year fixed mortgage being 7.19% in 2 years).

By waiting 2 years, it will cost the Whickham homeowner £174.11 extra per month in interest payments or £10,446.63 over the 5-year mortgage term.

The point is that because interest rates are forecast to go higher in the next couple of years, this provides potential Whickham buyers with the prospect of locking in their monthly housing expenses by moving now.

By buying now, it hedges against rising interest rates; consequently, your monthly mortgage payments are going to be higher. It offers an opportunity, through re-mortgaging, to lower your mortgage costs should interest rates fall.

What about Whickham first-time buyers?

I wrote an article on the Whickham property market only a few weeks ago. Even when we looked at house prices dropping by 18% in two years (because in the 1988 house price crash, the market dropped by 20% and 17% by 2008), the savings made on the purchase price were blown out of the water with the two extra years of rental payments, the higher deposit and higher interest payments.

The actual crisis in the property market today is the rocketing rental rates.

Whilst a fixed-rate mortgage locks in your monthly housing costs, rental rates are rocketing upwards, and a tenant today can realistically expect higher monthly costs in the coming few years.

Though most of the press generally focuses on the monetary aspects of buying a home, there are also choices on homeownership that are not exclusively based on financial decisions.

Why are you considering buying a Whickham home?

Buying a Whickham home is very personal and predominantly driven by your life events like divorce/marriage, a job move, a new addition to the family, elderly parents moving in etc. These are often the influences that drive the decision to buy (or not buy) a home.

Homeownership has always been a foundation stone of the

British dream.

Homeownership offers control and a sense of security that renting simply cannot provide.

The doom-monger headline-grabbing newspapers often overlook these non-economic factors affecting the desire of a potential home buyer.

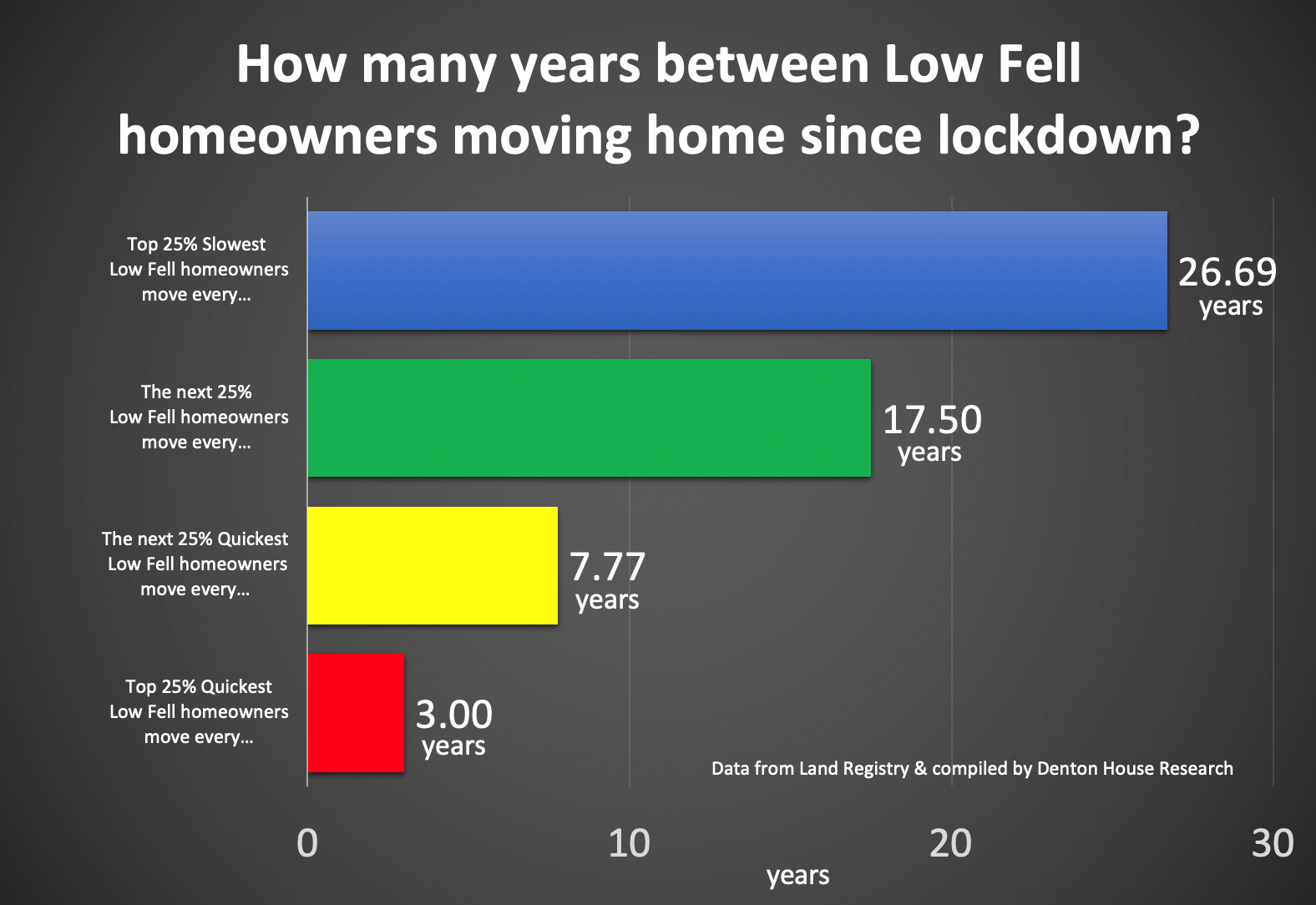

The one important thing from the last few years since the first lockdown in 2020 is that people still want to own their own homes.

They still want to have their ‘castle’, to pull up the drawbridge when things get tough, a place that they and their family can call their own. Never forget that homeownership is much more than house prices and graphs; it's about the ‘Englishman’s home is his castle’ dream.

Let us remember most people in the UK have been able to build and grow their family wealth through homeownership. That is why I like to provide the best information on the Whickham property market so you can make the best decision for yourself and your family. Please drop me a line if you wish to pick my brain on anything discussed in this article.

{kind=link}